The Government of India under the Finance Act, 2018 introduced a cess namely ‘Road and Infrastructure Cess’ under section 109 and 110 of the Finance Act, 2018 to be collected and levied on specified imported goods and on excisable goods as specified in the Sixth schedule of the said Act. The said goods are motor spirit commonly known as petrol and high-speed diesel oil. The rate specified under this schedule is Rs 8 per litre.

History and Reason for its Introduction:

- India has one of the largest road networks in the world that is used to transport over 60% of total goods and 85% of total passenger traffic. [Refer- Annual Report 2013-14, Ministry of Road Transport and Highways.]

- Seeing the opportunity of burgeoning demand of infrastructure, Cess was introduced in 1998-99 as a non-lapsable, dedicated fund to make roads. The non-lapsable pool of funds was subsequently adopted as a law under Central Road Fund (CRF) Act, 2000 (hereinafter referred as CRFA). The Funds to the CRFA were obtained from the cess imposed on petroleum products, diesel and petrol. An Additional Duty of Customs (import tax) and Additional Duty of Excise (tax on production) was also levied.

- The amendments to the Central Road Fund Act, 2000 has been brought through the Finance Act, 2018. The old provision is being substituted by the amended provision as referred below:

Old provision:

“the existing Central Road Fund governed by the Resolution of Parliament passed in 1988 for development and maintenance of National Highways and improvement of safety at railway crossing, and for these purposes levy and collect by way of cess, a duty of excise and a duty of customs on motor spirit commonly known as petrol, high speed diesel oil”,

The above provision is substituted by the Finance Act, 2018 as below:

“Central Road and Infrastructure Fund for development and maintenance of National Highways, railway projects, improvement of safety in railways, State and rural roads and other infrastructure, and for these purposes to levy and collect by way of cess, a duty of excise and a duty of customs on motor spirit commonly known as petrol and high speed diesel oil”

Introduction of Road and Infrastructure Cess:

The Finance Minister in his budget speech for the year 2018-2019, announced that the existing ‘Road Cess’ is been converted to the “Road and Infrastructure Cess”.

- Vide the above amendment, the ‘Road Cess’ is rechristened as “Road and Infrastructure cess”. The definition of Road and Infrastructure is wide as compared to the earlier definition of the “road” as in the CRFA. The list of activities that count as “infrastructure” are much wider under the amended CRFA. The funds can be used for various purposes such as national highways, rural roads, inter-State connectivities to other infrastructure projects etc.

- It is also to be noted that the size of this fund has grown over the years due to two factors—

(i) More vehicles on road (collected from users of diesel and petrol by levying an extra cess on the amount of fuel they bought)

(ii) Increasing the levy amount. - The windfall of revenue due to above reasons as well as amending the definition from ‘road fund’ to ‘road and infrastructure fund’ could propel India’s overall development and ensure time-bound creation of world-class infrastructure in the country.

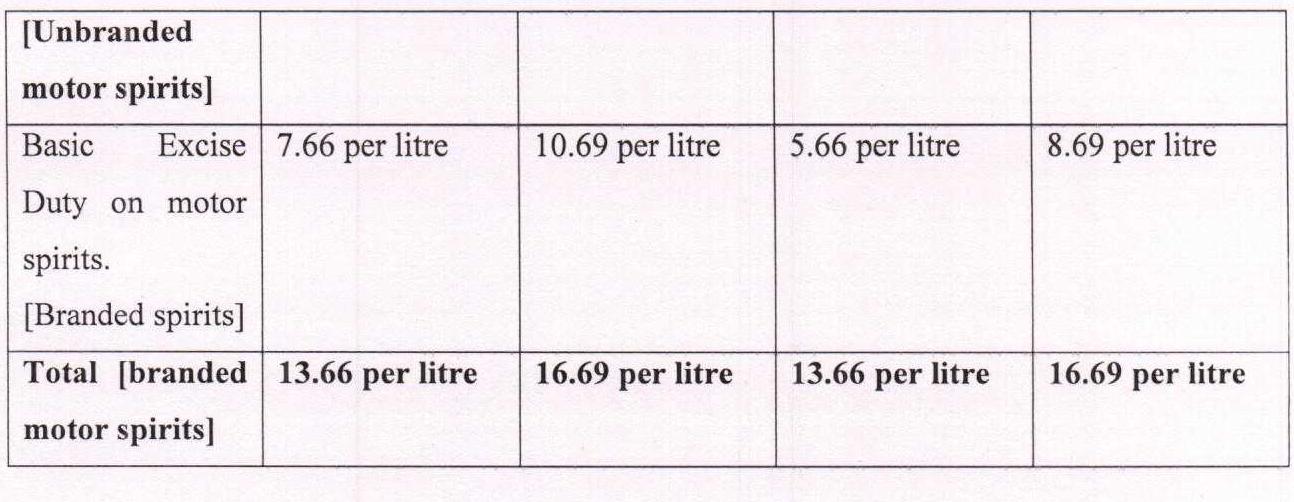

The comparative table is drawn below for finding the impact of the amended CRFA.

*With respect to Road and Infrastructure Cess @ 4 rupees per litre and the rate shall be effectively reduced.

Further, no Road and Infrastructure Cess are leviable on the following commodities where appropriate Excise duties & GST have been paid on the blending of such commodities:

- 5% ethanol blended petrol,

- 10% ethanol blended petrol and

- bio-diesel, up to 20% by volume.

In view of the above table and exemption, effectively there would be no additional burden of Road and Infrastructure Cess on the end users.

The above is for your information and updatation.

GST Law India is a blog on GST and allied commercial laws managed by members of the law firm ALA Legal.